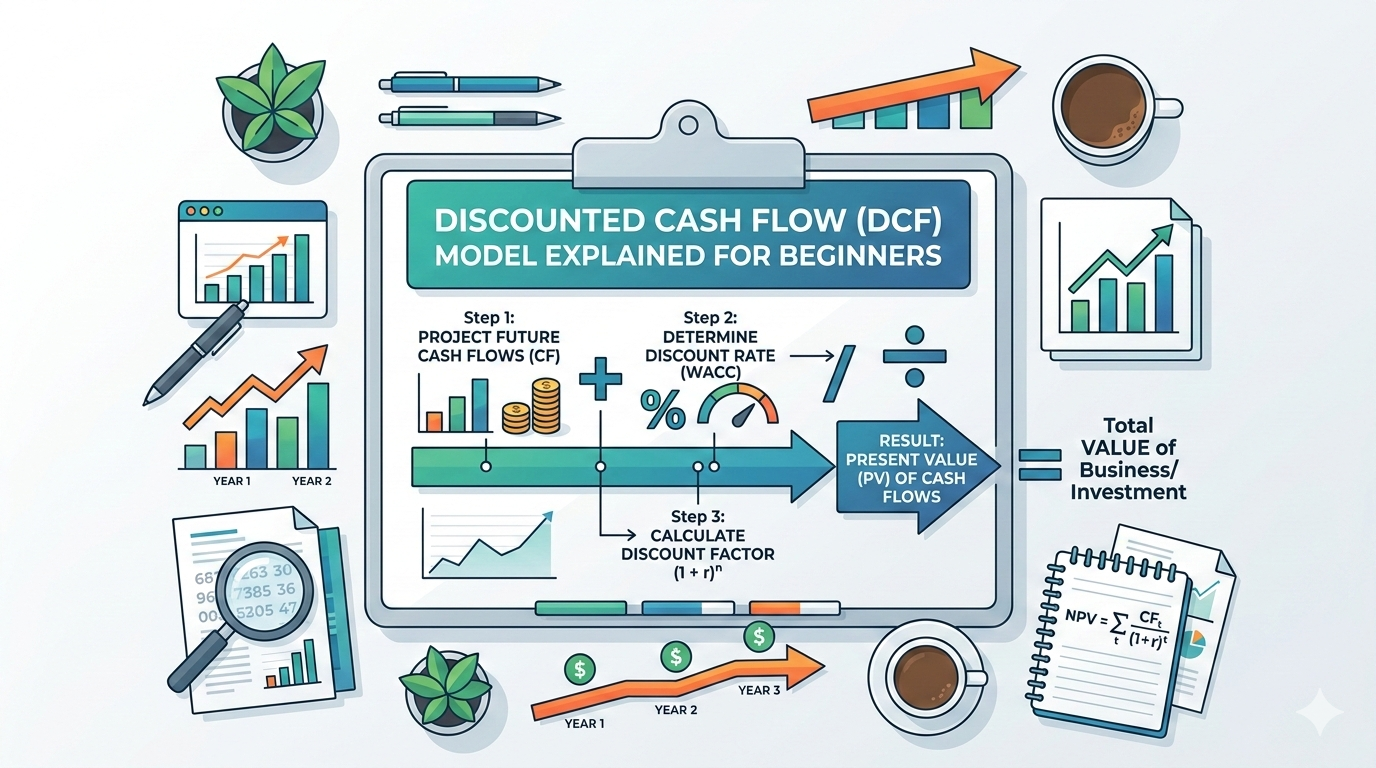

DCF Model Explained for Beginners

Learn the DCF model from scratch—no spreadsheets required. Understand intrinsic value, discount rates, and how to apply it to real stocks.

Intrinsic Alpha

Value Investing Research

Most retail investors avoid the DCF model because it looks like math. That fear costs them more than any bad stock pick ever will.

The investors who consistently beat the market aren't smarter — they're doing one thing differently. They attach a number to what a business is actually worth before they buy it. The DCF model is that number machine. And once you understand the logic, it's far less intimidating than your brokerage app's price chart.

This guide strips away the jargon. No finance degree required. No spreadsheet either.

What a DCF Model Actually Does

DCF stands for Discounted Cash Flow. The idea is brutally simple:

A business is worth the sum of all the cash it will ever generate — adjusted for the fact that money today is worth more than money tomorrow.

That's it. Every complexity you've heard about — WACC, terminal value, beta — is just an answer to one of the sub-questions inside that sentence.

The challenge isn't math. It's discipline. You have to make assumptions about the future, and those assumptions have to be grounded in business reality.

The Five Questions Every DCF Answers

You don't need a 40-tab model. You need honest answers to five questions:

- What is the business generating in free cash flow today?

- How fast will that cash grow — and for how long?

- What return rate do I require to take this risk?

- What is the business worth after my forecast period?

- How many shares does this value divide across?

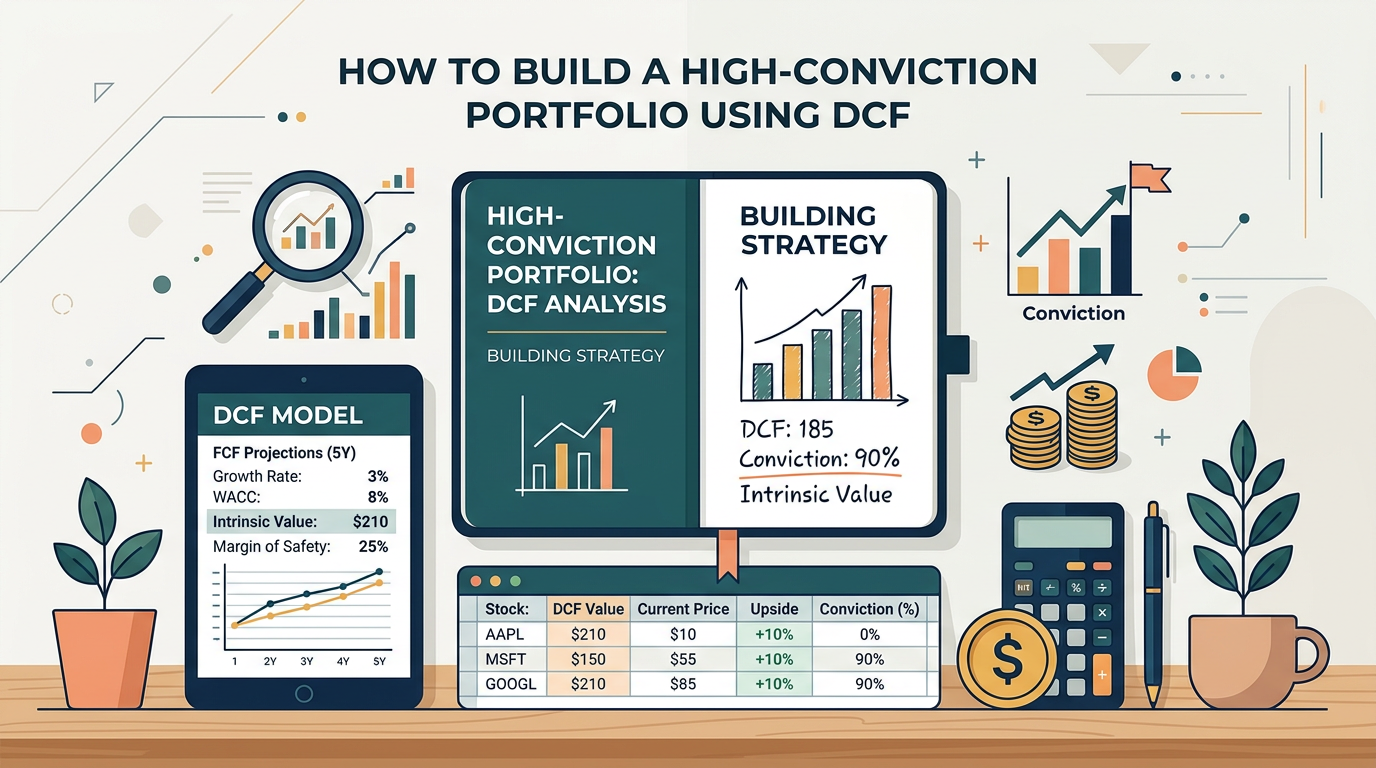

If you can answer those five questions with conviction, you have an intrinsic value estimate. The rest is rounding.

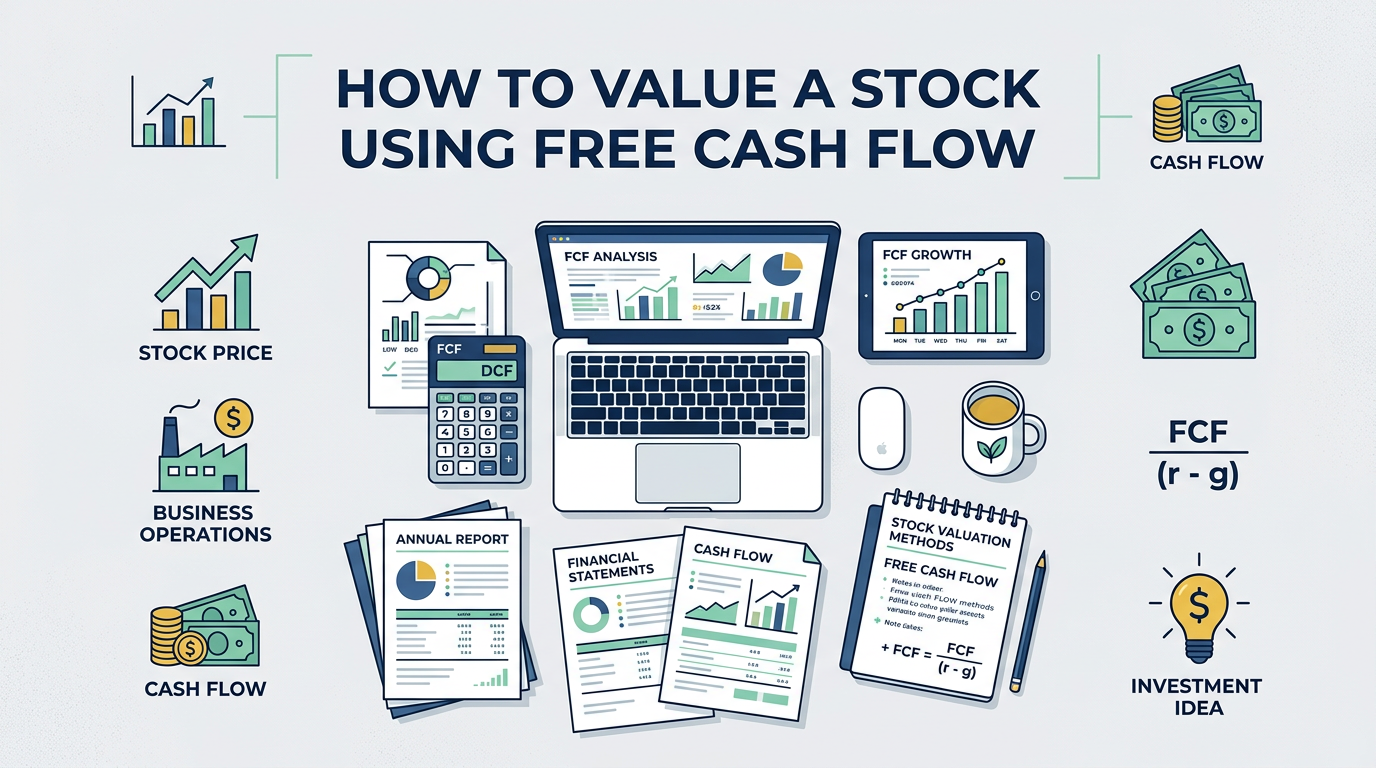

Step 1 — Start With Free Cash Flow

Free cash flow (FCF) is the lifeblood of a DCF. Not earnings. Not EBITDA. Cash.

FCF = Operating Cash Flow − Capital Expenditures

Why not earnings? Because accounting earnings include non-cash items and are subject to management judgment. Cash paid out to shareholders doesn't lie.

For cyclical businesses or companies with lumpy capex, use a normalized 3-year average of FCF instead of a single year. One exceptional year — in either direction — can destroy your entire valuation.

Step 2 — Project Cash Flow Growth

This is where beginners make their biggest mistake: using a single growth rate across the entire forecast.

Real businesses don't grow linearly. A better structure:

- Years 1–5: Higher, analyst-supported growth rate

- Years 6–10: Fade toward a more mature, sustainable rate

- Terminal year: Converge to a long-run rate near GDP growth (2–3%)

Counter-intuitive insight: The terminal growth rate matters far more than your near-term growth assumption. A difference of 1% in terminal growth can move your intrinsic value estimate by 20–30%. Most beginners obsess over the wrong input.

Step 3 — Choose a Discount Rate

The discount rate is your required annual return. It answers the question: what return do I need to accept this risk?

Most retail investors use a flat hurdle rate — typically 9–12% — rather than a calculated WACC. This approach is defensible and avoids the false precision of plugging in a "market-derived" beta that changes every month.

The formula to bring future cash flows back to today:

PV = FCFₙ ∕ (1 + r)ⁿ

Where r is your discount rate and n is the year. A dollar 10 years from now, discounted at 10%, is worth about $0.39 today.

Step 4 — Calculate Terminal Value

The terminal value captures everything beyond your forecast window. In most models, it represents 60–80% of the total intrinsic value estimate. That number should give you pause.

The perpetuity growth formula:

TV = FCF(N+1) ∕ (r − g)

Where g is the assumed growth rate into perpetuity. Set this conservatively — 2% to 3%. If you're modeling a company growing at 2.5x GDP forever, you're not modeling a business, you're modeling a fantasy.

Step 5 — Bridge to Per-Share Value

Enterprise value tells you what the whole business is worth. You need equity value — what belongs to shareholders.

Equity Value = Enterprise Value + Cash − Debt

Intrinsic Value Per Share = Equity Value ∕ Diluted Shares Outstanding

Always use diluted share count. Stock-based compensation is real dilution. Companies that issue options aggressively are transferring value from existing shareholders — something the price chart will never show you.

Free Cash Flow: The Foundation of Every Honest Valuation

Free cash flow consistency is a quality signal, not just a valuation input. Businesses that grow FCF reliably over a decade tend to compound at rates that look impossible in retrospect. The DCF model forces you to look at that track record and project it honestly.

The Reverse DCF — What the Market Is Already Pricing In

Here's the insight that separates institutional analysts from retail investors: instead of building a DCF forward from your assumptions, run it backward from the current price.

The question becomes: what growth rate is the market implying at today's valuation?

If the stock price implies 18% annual FCF growth for the next ten years, you don't need to predict the future — you just need to decide if that's realistic. This reframes valuation from prediction to judgment.

This is the most powerful beginner tool that almost nobody uses.

Intrinsic Value Estimate

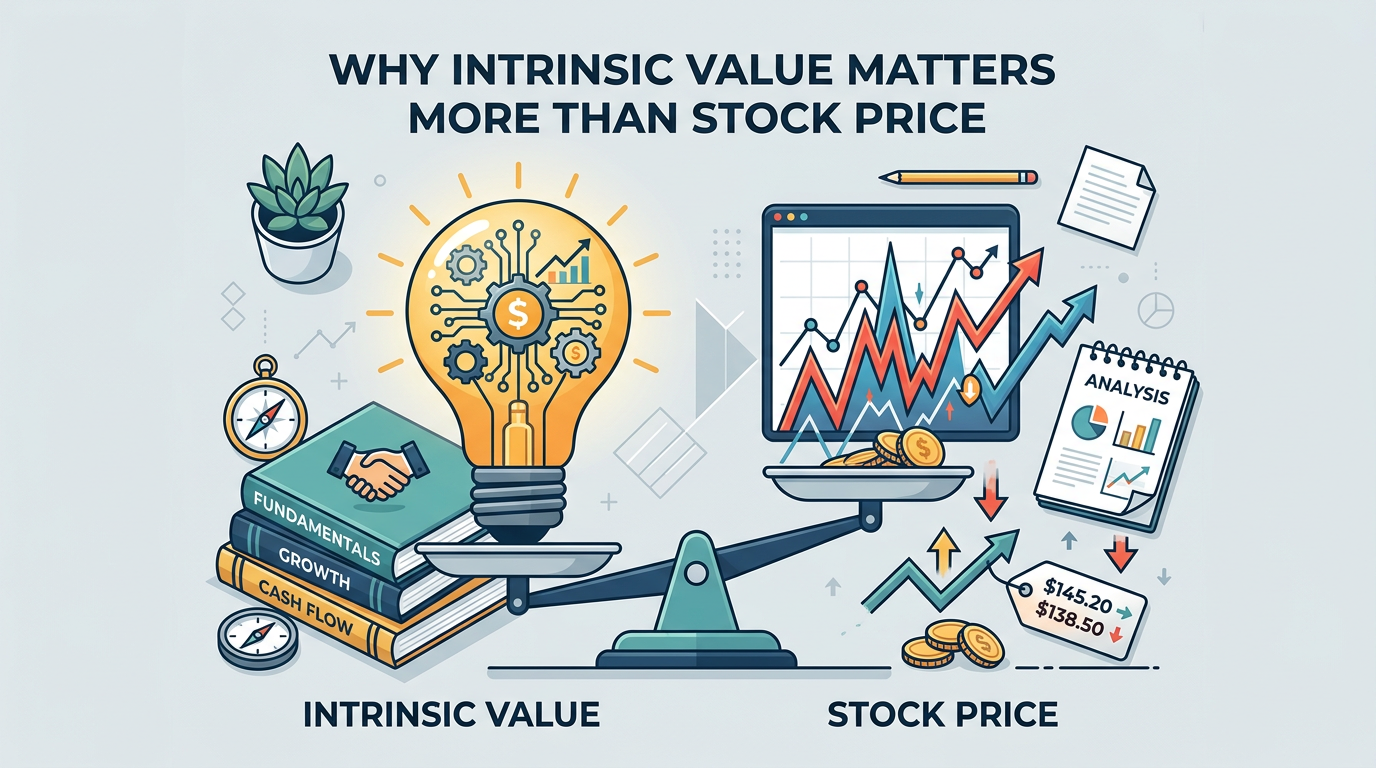

Margin of Safety: Why Your DCF Estimate Is Never the Buy Price

A DCF model outputs an estimate — not a fact. You're making assumptions about the future, and the future is wrong about itself constantly.

The margin of safety is your buffer against being wrong:

- Conservative investors: 30–50% below intrinsic value

- Growth investors: 10–20% below, if the business quality is high

- No margin of safety: You're speculating, not investing

Benjamin Graham framed this simply: "The margin of safety is always dependent on the price paid." The DCF tells you the value. The stock market tells you the price. The gap between them is either your opportunity or your warning.

Capital Allocation: The Variable Most Beginners Ignore

Your DCF model implicitly trusts management to deploy retained earnings at rates that justify the discount rate you've applied. That's a serious assumption.

Questions a rigorous DCF forces you to ask:

- Is the company buying back shares at prices above intrinsic value? (Value destruction)

- Are acquisitions generating returns above the cost of capital?

- Is capex sustaining an existing moat or building a new one?

A business with excellent FCF generation but poor capital allocation can be worth far less than the model implies. The cash flow matters. What they do with it matters more.

Full Analysis Checklist

Common Beginner Mistakes

- Using EPS instead of FCF — earnings are opinions, cash is a fact

- Single-stage growth models — real businesses have phases, not constants

- Ignoring share dilution — SBC reduces your ownership silently

- Anchoring to the current price — the price is an input to nothing; the value is

- Skipping the margin of safety — precision without humility is dangerous

The Best DCF Is a Simple One You'll Actually Run

The perfect model that you never open is worthless. A simple, honest model run consistently across every investment idea you evaluate is one of the most powerful edges available to retail investors.

You don't need Bloomberg. You don't need a 40-tab Excel file. You need five honest inputs, a conservative bias, and the discipline to buy below your estimate of value.

That's the whole game. Everything else is noise.